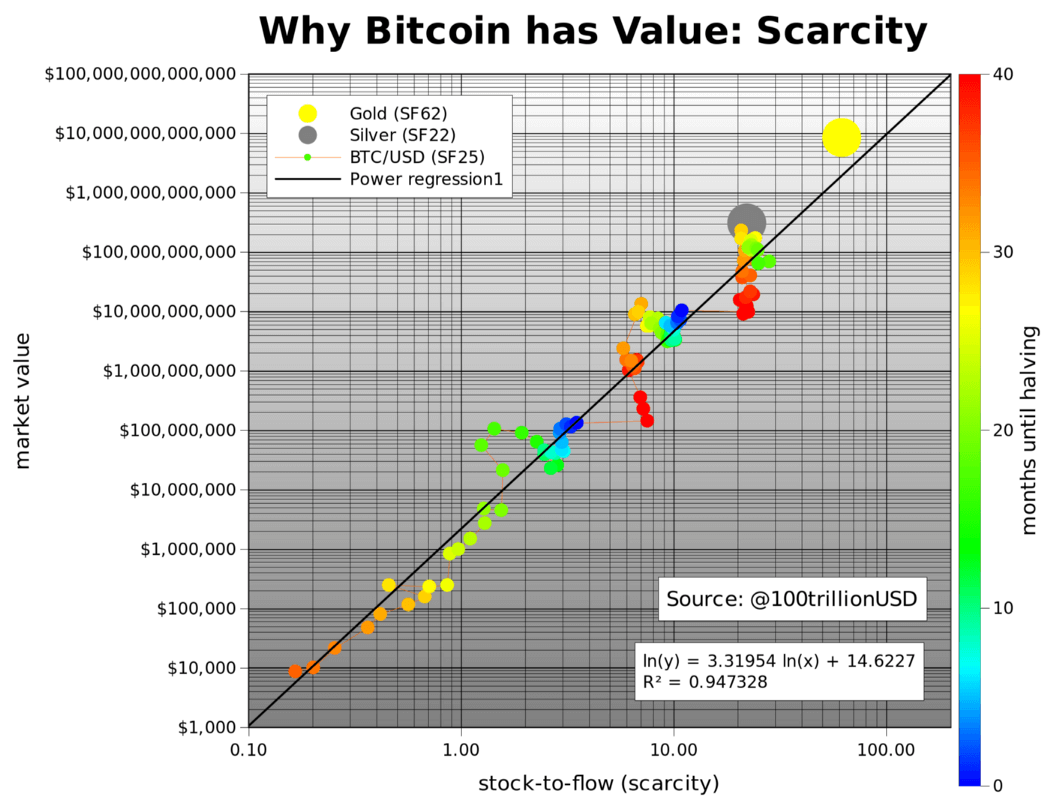

If you zoom out the price chart, you will see that Bitcoin has been steadily going up in value since it was created, trading at less than $0.01 and slowly climbing to over $20,000 USD at its most recent peak at the end of 2017.

This is because its supply is fixed and people value its scarcity. With more demand and a fixed supply, prices go up over time. As the years go on, its value will continue to increase as new users start holding Bitcoin.

Original Source written by BitcoinQ_A